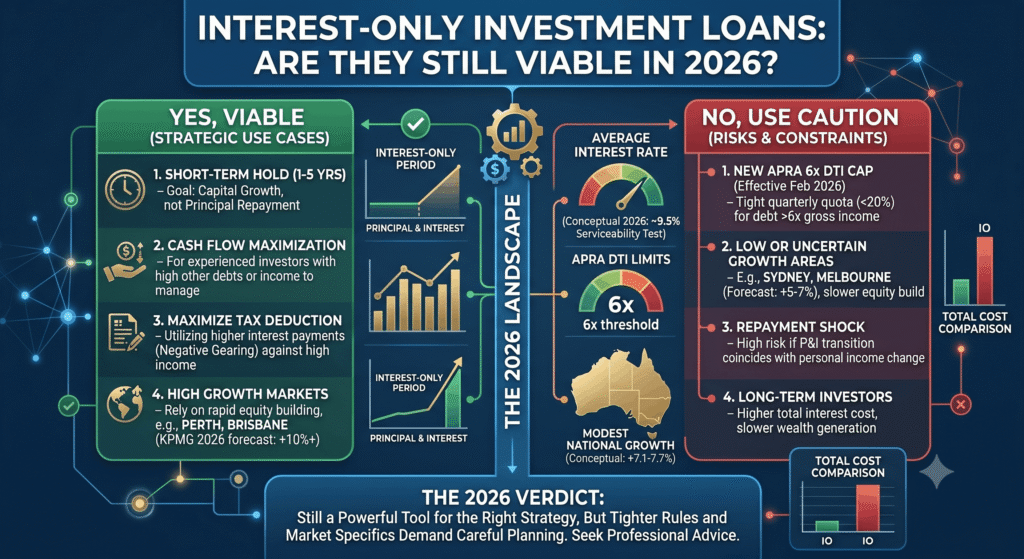

For years, interest-only loans were the not-so-secret weapon of Australian property investors. Pay only the interest, keep your repayments low, maximise your tax deductions, and let capital growth do the heavy lifting. It was the engine behind countless property portfolios.

But 2026 looks very different. Interest rates rose again early this year, the era of cheap money is well and truly over, and from 1 July 2027 the government’s negative gearing reforms will rewrite the tax playbook that made interest-only so attractive in the first place. So the question every investor is now asking is fair: is an interest-only investment loan still a smart move — or a relic of a cheaper era?

This guide answers that in plain English. We’ll explain how interest-only investment loans actually work, weigh the advantages against the real risks, walk through interest-only vs principal and interest with worked repayment examples, and cover the tax, cash flow, borrowing capacity and APRA angles every investor needs in 2026. Then we’ll show exactly when interest-only still makes sense — and when it doesn’t. Let’s get into it.

What Is an Interest-Only Investment Loan?

An interest-only investment loan is a mortgage where, for a set period, you only repay the interest charged — not any of the amount you borrowed (the principal).

Plain-English definition:

- Principal = the amount you borrowed.

- Interest = what the lender charges you to borrow it.

- Interest-only = for a fixed period, you pay only the interest, so the loan balance doesn’t reduce.

With a standard principal-and-interest (P&I) loan, every repayment chips away at both the interest and the loan balance, so you build equity from day one. With interest-only (IO), your repayments are lower — but your debt stays exactly the same.

How long does the interest-only period last?

In Australia, IO periods for investors are typically capped at 5 years (sometimes shorter). At the end of that period, the loan automatically reverts to principal-and-interest — and here’s the catch most beginners miss: you now have to repay the full original balance over the remaining term (often 25 years instead of 30). That compresses the repayment and pushes it up sharply. More on this “repayment shock” below.

Interest-only is overwhelmingly an investor product: around 29% of outstanding investor loans are interest-only, compared with roughly 3% of owner-occupier loans.

Interest-Only vs Principal-and-Interest: Side-by-Side

| Feature | Interest-Only (IO) | Principal-and-Interest (P&I) |

|---|---|---|

| Monthly repayment | Lower (interest only) | Higher (interest + principal) |

| Builds equity? | No — balance stays flat | Yes — from day one |

| Interest rate | Slightly higher (investors ~0.2% more) | Lower |

| Total interest paid | More over the life of the loan | Less |

| Cash flow | Maximised | Tighter |

| Tax-deductible interest | Stays high (good for investors) | Falls as balance reduces |

| Best suited to | Cash-flow-focused investors, debt recyclers | Long-term debt reduction, owner-occupiers |

A worked repayment example

Let’s use a $600,000 investment loan at 6.6% (indicative investor rates in 2026 sit roughly 6.6%–6.9%, depending on LVR and lender):

- Interest-only repayment: about $3,300 per month

- Principal-and-interest repayment (30-year term): about $3,832 per month

- Monthly difference: roughly $530 lower with interest-only

That $530 a month ($6,360 a year) is the cash-flow benefit investors chase. But remember — with IO, after five years you still owe the full $600,000.

The reversion shock

When the 5-year IO period ends, that $600,000 must now be repaid over the remaining 25 years:

- New P&I repayment: about $4,089 per month

- That’s roughly $789 more per month than the IO repayment you’d grown used to.

This jump is the single biggest risk of interest-only lending — and the reason you must plan for it before you sign, not when the letter arrives.

The Advantages of Interest-Only Investment Loans

- Maximised cash flow. Lower repayments free up money each month — useful for holding costs, buffers, or funding the next deposit.

- Higher tax-deductible interest. Because the balance doesn’t fall, your interest (which is tax-deductible on an investment property) stays high. P&I, by contrast, sees your deductible interest shrink over time.

- Flexibility for portfolio building. Lower outgoings can help you service and hold more properties while you build equity through growth.

- Pairs powerfully with an offset account. You can park surplus cash (including what would have been principal repayments) in an offset to reduce interest — while keeping that money accessible (more below).

- Supports debt recycling. A common strategy: keep your investment (tax-deductible) loan on IO, and direct the cash you save into paying down your home loan (non-deductible “bad debt”) faster.

The Disadvantages and Risks

Interest-only isn’t free money — it’s a trade-off. The downsides are real, especially in 2026.

1. The repayment shock

As the example showed, repayments can jump hundreds of dollars a month when the IO period ends. Investors who didn’t plan for it can be caught badly short — particularly with rates already elevated.

2. Refinancing risk

Many investors plan to simply refinance into a fresh IO period when the first one ends. But that’s not guaranteed. In a tighter lending environment, you must requalify — and if your income has dropped, rates have risen, or lending rules have tightened (they have), you may be stuck reverting to P&I whether you like it or not. Relying on being able to refinance is a risk, not a plan.

3. You pay more interest overall

Because you’re not reducing the balance during the IO period, you pay interest on the full amount for longer — meaning more total interest over the life of the loan.

4. No equity built through repayments

With IO, your equity growth depends entirely on the property’s value rising. If the market stalls or falls, you’ve built nothing through your repayments — and could even face negative equity.

Tax Implications and Negative Gearing

This is where interest-only has always shone for investors — and where 2027 changes the game.

On an investment property, the interest portion of your loan is generally tax-deductible, while principal repayments are not. Because interest-only keeps your loan balance (and therefore your deductible interest) high, it has traditionally maximised the tax benefit — a natural fit with a negative gearing strategy, where you offset rental losses against your income.

Plain-English definition — Negative gearing: When the costs of owning an investment property (including interest) exceed the rent it earns, creating a loss that has, until now, been deductible against your other income.

⚠️ The 2027 reform you must factor in

In the 2026–27 Federal Budget (announced 12 May 2026), the government announced that from 1 July 2027:

- Negative gearing on established residential properties bought after 7:30pm on 12 May 2026 will be limited — losses will only be deductible against rental income or capital gains from rental properties, not your salary.

- Properties already held before that date are grandfathered, and new builds remain exempt (keeping both negative gearing and the existing CGT discount).

- The 50% capital gains tax discount is being replaced with an inflation-based system plus a minimum 30% tax on gains, for gains after 1 July 2027.

These measures are not yet law, but the implication for interest-only investors is significant: the classic “interest-only + negative gearing against salary” strategy is being narrowed for new purchases of established homes. New builds keep the advantage. As always, get current advice from a licensed accountant.

Cash Flow Benefits and Offset Accounts

The smartest interest-only investors don’t just pocket the cash-flow saving — they put it to work, usually through an offset account.

Plain-English definition — Offset account: A transaction account linked to your loan. Money sitting in it is “offset” against your loan balance, so you only pay interest on the difference. Keep $50,000 in an offset against a $600,000 IO loan and you only pay interest on $550,000 — while that cash stays fully accessible.

The power move: take the money you’d otherwise put toward principal and park it in the offset instead. You reduce your interest (just like P&I would) but keep the flexibility to pull that cash out for the next deposit, an emergency, or your own home loan. You get the discipline of P&I with the flexibility of IO.

A common structure sophisticated investors use is a split loan — fixing a portion of the debt for repayment certainty while keeping the rest variable with an offset for tax planning and flexibility. Discuss the right structure with your broker and accountant.

Borrowing Capacity and APRA Rules in 2026

Two regulatory realities shape property investor finance today.

First, the APRA serviceability buffer remains at 3%. Lenders must check you could still afford repayments at 3 percentage points above the actual rate — so with investor rates around 6.5%+, you’re assessed near 9.5%. This alone cuts borrowing capacity by an estimated 15–20%.

Second — and crucial for IO — lenders assess interest-only loans on the higher P&I repayments over the residual term. In other words, the bank doesn’t size your loan on the low IO repayment; it sizes it on what you’ll pay after the IO period ends, squeezed into the shorter remaining term. This makes interest-only loans harder to qualify for, not easier, despite the lower actual repayments.

There’s also a new debt-to-income (DTI) “speed limit” from February 2026: banks can issue no more than 20% of new loans to borrowers with total debt above six times their gross income — a real ceiling for investors stacking multiple loans.

One myth to bust: You may read that “banks must cap interest-only at 30% of new lending.” That APRA restriction existed from 2017 but was removed in January 2019. Interest-only lending is freely available again in 2026 — the constraints today are serviceability and DTI, not a blanket IO cap.

When Interest-Only Still Makes Sense in 2026

Interest-only remains a viable, smart tool — for the right investor, in the right situation:

- You’re cash-flow focused and disciplined. You’ll use the saving productively (offset, buffers, paying down bad debt) — not just spend it.

- You’re a debt recycler. You have a non-deductible home loan to attack while keeping investment debt high and deductible.

- You’re building a portfolio and need to preserve cash flow to hold multiple properties while equity grows.

- You invest in new builds and want to retain negative-gearing benefits under the post-2027 rules.

- You have a genuine plan for the reversion — you know what the P&I repayment will be and can afford it (or have an offset balance ready to cushion it).

- You’re managing a temporary squeeze — IO can be a short-term cash-flow relief valve in an emergency.

When to think twice

- You’re relying on being able to refinance into another IO period (not guaranteed).

- You have no plan for the repayment shock.

- You won’t use the cash-flow saving productively.

- Your strategy depends entirely on negative gearing against salary for a new established property bought after 12 May 2026.

Real Australian Investor Scenarios

Scenario 1: The disciplined portfolio builder (IO makes sense)

Aisha, 39, owns two investment properties and is building toward five.

She uses interest-only to keep her portfolio cash-flow healthy, parking surplus cash in offset accounts against each loan. The lower repayments protect her serviceability so she can keep buying, while the offset balances quietly reduce her interest. She knows exactly what each loan reverts to and keeps buffers ready. Interest-only is doing real work for her.

Scenario 2: The debt recycler (IO makes sense)

Tom, 47, still owes $300,000 on his (non-deductible) family home.

He keeps his $550,000 investment loan on interest-only — minimising those repayments — and channels every spare dollar into his home loan, his only “bad” debt. He’s killing non-deductible debt fast while keeping his deductible investment debt high. A textbook use of interest-only.

Scenario 3: The hopeful flipper with no plan (IO is risky)

Jess, 28, took interest-only purely to afford a property she’s betting will rise, planning to “just refinance” in five years.

If growth stalls or her income dips, she can’t requalify, gets forced onto P&I, and faces a repayment jump she didn’t budget for. Interest-only without a plan is a trap, not a strategy.

Actionable Tips for Interest-Only Investors in 2026

- Always model the reversion repayment before you sign. Know the post-IO P&I figure and confirm you can afford it.

- Pair IO with an offset account and actually use it — discipline turns IO from risky to powerful.

- Don’t rely on refinancing. Treat another IO period as a bonus, not the plan.

- Use IO to attack non-deductible debt first (your home loan) if you have it.

- Keep a cash buffer of several months’ repayments per property — essential with rates elevated.

- Get tax advice on the 2027 changes before buying established property, and consider new builds if negative gearing matters to your strategy.

- Use a portfolio-savvy broker. Lenders assess IO serviceability very differently — the right lender can make or break your application.

- Review your structure regularly. What suited you at 6% may not suit you after the next rate move.

Frequently Asked Questions

Are interest-only investment loans still worth it in 2026? Yes — for disciplined, strategy-driven investors who use the cash-flow saving productively (offset, buffers, debt recycling) and plan for the reversion to P&I. They’re riskier for those relying on refinancing or with no plan for the repayment jump.

What’s the difference between interest-only and principal-and-interest? With interest-only you repay only the interest for a set period, so the balance doesn’t reduce and repayments are lower. With principal-and-interest you repay both, building equity from day one with lower total interest over the loan’s life.

How long can an interest-only period last in Australia? Typically up to 5 years for investors, after which the loan reverts to principal-and-interest over the remaining term — which raises repayments, often sharply.

Are interest-only loans more expensive? The interest rate is usually slightly higher (for investors, often around 0.2% above P&I), and because you don’t reduce the balance, you pay more total interest over the life of the loan.

Can I still get an interest-only loan after the APRA changes? Yes. APRA’s old 30% cap on interest-only lending was removed in January 2019. Interest-only is available in 2026 — the real constraints are the 3% serviceability buffer, strict IO assessment (on the higher post-IO repayments), and the new 6× debt-to-income cap.

Do interest-only loans help with negative gearing? Historically, yes — they keep your tax-deductible interest high. But from 1 July 2027 (not yet law), negative gearing on established homes bought after 12 May 2026 is set to be limited; new builds remain exempt. Seek current accounting advice.

What happens if I can’t afford the repayments when interest-only ends? Options include refinancing (if you qualify), extending or requesting a new IO period (not guaranteed), selling, or drawing on an offset buffer. The safest approach is to plan for the reversion before it arrives.

The Bottom Line: A Powerful Tool, Not a Shortcut

So — are interest-only investment loans still viable in 2026? Yes, but only as a deliberate strategy, not a way to simply afford more property.

In a higher-rate, reform-shaped market, interest-only rewards the disciplined investor: the one who funnels the cash-flow saving into an offset, attacks non-deductible debt, keeps real buffers, and knows exactly what their repayments revert to. It punishes the investor who treats it as easy money and hopes to refinance their way out later.

The fundamentals of smart investment property loan Australia strategy haven’t changed: structure your finance around your goals, plan for every scenario, and never borrow on hope. Interest-only is a precision tool — invaluable in the right hands, dangerous in the wrong ones.

Your next step: Before your interest-only period starts (or ends), do one thing this week — ask your broker or use a loan calculator to work out your exact reversion repayment, then confirm you could comfortably afford it today. If yes, interest-only may be a smart part of your plan. If not, that’s your answer. Either way, sit down with a portfolio-experienced broker and an investment-focused accountant — especially with the 2027 tax changes on the horizon — and structure your loans around the wealth you’re actually trying to build.

Disclaimer: This article is general information only and does not constitute financial, tax, legal or credit advice. It does not take into account your personal circumstances, objectives or needs. Interest rates, lending criteria, APRA settings and tax laws change frequently, and the figures here (including indicative 2026 rates and repayment examples) are illustrative only. The negative gearing and CGT measures referred to were announced as at the 2026–27 Federal Budget and are not yet law as at the date of writing. Property investment and borrowing carry risk, including the risk of loss. Always seek advice from a licensed mortgage broker, financial adviser and/or accountant before making any borrowing or investment decision.