Here’s something most Australian homeowners don’t realise: you may already be sitting on the deposit for your next property — locked inside the walls of the home you live in.

As your home rises in value and you chip away at your mortgage, you build up equity. And that equity isn’t just a number on paper — used wisely, it can become the deposit and purchasing costs for an investment property, without you saving another dollar. This single strategy is how a huge number of Australians go from one property to a portfolio.

But equity release is powerful in both directions. Done well, it’s the engine of wealth creation. Done badly — over-leveraged, with no buffer, tangled across loans — it’s how people get into trouble. And in 2026, with interest rates higher and lending tighter, getting it right matters more than ever.

This guide explains equity release in Australia in plain English: what home equity is, how to work out how much you can actually use, the methods to access it (refinancing, redraw, offset and more), and a step-by-step example of how to use equity to buy an investment property. We’ll cover the risks, the common mistakes, and the strategies for building a portfolio safely. Let’s unlock it.

What Is Home Equity?

Home equity is the portion of your property you truly own — its current market value minus whatever you still owe on it.

Home equity = Property value − Loan balance

For example, if your home is worth $900,000 and you owe $400,000 on your mortgage, you have $500,000 in equity.

Equity grows two ways: as your property value rises (capital growth), and as you pay down your loan. The good news? You don’t have to sell to put that equity to work — which is where equity release comes in.

What Is Equity Release?

Equity release simply means accessing some of the equity in a property you already own, turning it into usable funds — typically by restructuring or topping up your loan. Investors most often use it to fund the deposit and purchasing costs for their next property.

In one sentence: Equity release lets you borrow against the value you’ve built in your home and use that money as the deposit for an investment property — so your existing property helps buy the next one.

A quick clarification: “Equity release” can also refer to reverse mortgages or the government’s Home Equity Access Scheme, which let retirees draw on their home’s value for income without repayments. That’s a different product for a different purpose. This guide is about the investor strategy — using equity to buy more property — not reverse mortgages.

Usable Equity: The Number That Actually Matters

Here’s the catch that trips up beginners: you can’t access all your equity. Lenders won’t let you borrow against 100% of your home’s value. The figure that matters is usable equity.

LVR explained

Lenders think in terms of Loan-to-Value Ratio (LVR) — how much you’re borrowing against a property’s value.

LVR = (Loan amount ÷ Property value) × 100

Most lenders let you borrow up to 80% of a property’s value without charging Lenders Mortgage Insurance (LMI). Push above 80% and LMI kicks in — an extra cost that protects the lender, not you.

The usable equity formula

Because lenders cap borrowing at around 80%, your usable equity is:

Usable equity ≈ (Property value × 80%) − Current loan balance

Worked example

Back to our homeowner with a $900,000 home and a $400,000 loan:

- 80% of $900,000 = $720,000

- Minus the existing loan of $400,000

- Usable equity = $320,000

So while their total equity is $500,000, their usable equity — the amount they can realistically tap for an investment — is around $320,000. (You can sometimes access equity above 80% by paying LMI, but most investors stay at or under 80% to avoid the cost.)

That $320,000 is more than enough to fund the deposit and costs on a typical investment property — and possibly more than one.

How to Access Your Equity: 4 Methods Compared

There are several ways to release equity. Each works differently and suits different goals.

| Method | How it works | Best for | Watch out for |

|---|---|---|---|

| Refinance / loan top-up (cash-out) | Increase your existing loan (or switch lenders) and take the extra as a separate split | Funding a deposit + costs for a purchase | Requalifying under current rules; new rate |

| Redraw facility | Pull back extra repayments you’ve made on your loan | Quick access to your own prepaid funds | Tax “purpose” issues — can contaminate deductibility |

| Offset account | Cash held in an account that offsets your loan balance | Keeping funds flexible and accessible | Doesn’t increase your borrowing — it’s your cash |

| Line of credit / equity loan | A pre-approved limit you draw on as needed | Investors making multiple/ongoing purchases | Higher rates; discipline required |

Refinancing (the most common route)

Refinancing an investment property purchase usually means increasing your home loan (or moving to a new lender) and taking the released equity as a separate loan split — for example, a new $150,000 split specifically for the deposit and costs on your investment. This keeps the borrowing clean and the purpose clear (important for tax).

Redraw facility

A redraw lets you withdraw extra repayments you’ve made above your minimum. It’s handy — but there’s a serious tax trap: the deductibility of interest depends on what the borrowed money is used for. Pulling funds out of your home loan via redraw to buy an investment can create a “mixed-purpose” loan that’s messy to apportion at tax time. A clean, separate loan split is almost always better. Get advice from your accountant before using redraw this way.

Offset account

An offset account is a transaction account linked to your loan; the balance “offsets” your loan, so you pay interest on less. It’s a brilliant flexibility tool — but remember, an offset holds your cash. It doesn’t create new borrowing capacity. Many investors keep released-equity funds in an offset until they’re ready to deploy them.

Line of credit / home equity loan

A home equity loan Australia-style line of credit gives you a pre-approved limit to draw on as needed — useful for serial investors making multiple purchases. The trade-offs are typically higher interest rates and the discipline required not to overspend.

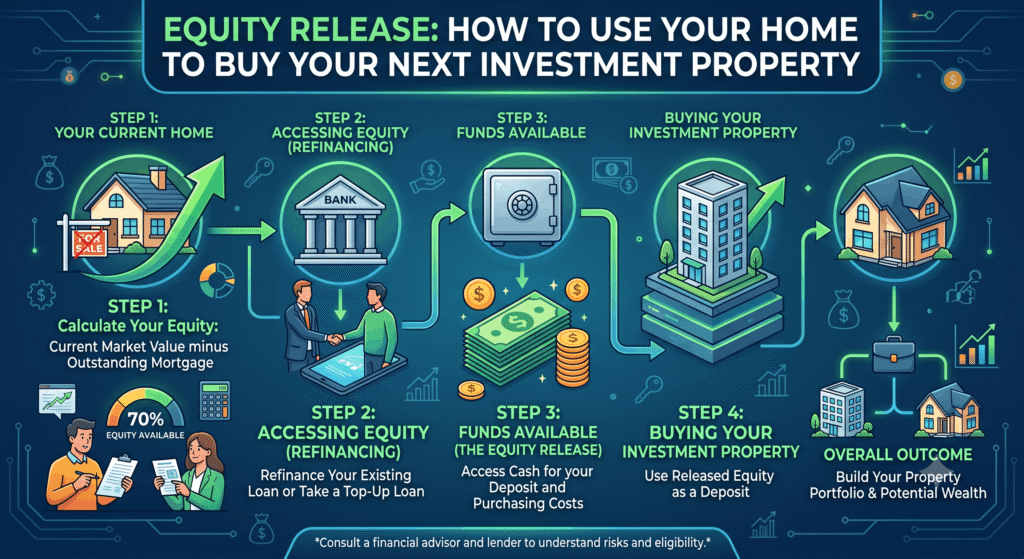

Step-by-Step: Using Equity to Buy Your Next Investment Property

Here’s how the strategy works in practice, using our $900,000 home / $320,000 usable equity example.

Step 1: Get your property valued

Your lender arranges a valuation to confirm your home’s current market value — this sets your usable equity. (Values can come in lower than you hope, so don’t over-plan.)

Step 2: Calculate your usable equity

Property value × 80% − loan balance. In our case: $320,000 usable.

Step 3: Confirm your borrowing capacity

Usable equity gets you the deposit, but you still need the serviceability to support a second loan. The bank checks you can afford both loans under its rules (more below). Equity without borrowing capacity gets you nowhere — both must line up.

Step 4: Set up a separate equity loan split

Release, say, $150,000 as a new loan split secured against your home — enough for a 20% deposit plus stamp duty, legals and buying costs on a ~$600,000 investment property. Keeping it as a separate split (not mixed into your home loan) keeps the tax treatment clean.

Step 5: Buy the investment with a standalone loan

Take a separate 80% loan ($480,000) secured against the new investment property itself. Combined with your $150,000 equity split, that funds the full purchase.

Why two separate loans? This structure avoids cross-collateralisation — tangling both properties as security for each other. Keeping loans standalone means you can sell or refinance one property without the other getting caught up, and you’re not locked to a single lender. It’s the single most important structural decision when building a portfolio with equity.

Step 6: Manage cash flow and repeat

As both properties grow in value, you build new usable equity — which can fund property number three, and so on. This is the chain reaction (often called equity recycling) that turns one home into a portfolio.

Borrowing Capacity and Lender Requirements in 2026

Equity is only half the equation. In 2026, the lending environment is the other half — and it’s tighter than the boom years.

- The APRA serviceability buffer is 3%. Lenders assess whether you could afford repayments at 3 percentage points above the actual rate — so with investor rates around 6.5%+, you’re tested near 9.5%. This cuts borrowing capacity by an estimated 15–20%.

- A new debt-to-income (DTI) cap applies from February 2026. Banks can issue no more than 20% of new loans to borrowers whose total debt exceeds six times gross income. Releasing equity adds to your debt — so it pushes your DTI up, potentially toward this ceiling.

- The 80% LVR sweet spot. Stay at or under 80% combined LVR to avoid LMI on the equity you release.

- You must requalify. Refinancing or topping up means a fresh serviceability assessment at current rates and rules. If your income has changed, you may release less than you expect.

- Rental income helps. Lenders count a portion of the expected rent (often shaded to ~80%) toward your serviceability — which can make the second loan more achievable.

The reality check: Two households with identical equity can have very different outcomes depending on income, existing debts, DTI and which lender they use. A portfolio-savvy broker is worth their weight here.

Cash Flow Considerations

Releasing equity increases your total borrowings — which means higher total repayments. Before you buy, make sure the numbers work month to month:

- Will the rent cover most of the new property’s costs? Calculate the net position after the loan repayments, rates, insurance, management and maintenance.

- Can you absorb a shortfall if the property is negatively geared, or a vacancy hits?

- Have you kept a buffer? Don’t release every last dollar of equity — keep a cash reserve (ideally in an offset) of several months’ repayments per property.

- Have you stress-tested at a higher rate? Rates rose again in early 2026; assume they can move further.

The Risks of Equity Release

Used carelessly, equity release amplifies risk as much as reward:

- You’re increasing debt against your home. Your family home becomes security for investment borrowing — if things go wrong, that’s a serious consequence.

- Over-leverage. Releasing too much equity with no buffer leaves you exposed to rate rises, vacancies and value falls.

- Falling values / negative equity. If your home’s value drops after you’ve released equity, your combined LVR climbs and your options shrink.

- Cross-collateralisation traps. Tangling properties as shared security can lock you to one lender and complicate selling.

- Tax contamination. Using redraw or mixed loans incorrectly can muddy your interest deductibility — get advice.

- The 2027 tax changes. From 1 July 2027 (not yet law), negative gearing on established homes bought after 12 May 2026 is set to be limited to rental income/capital gains, while new builds stay exempt, and the 50% CGT discount is being replaced. Factor this into the strategy and seek current advice.

Real Australian Investor Scenarios

Scenario 1: The first-time investor (equity unlocks the door)

Priya and Sam own a $900,000 home with a $400,000 loan — but only $20,000 in savings.

They thought they couldn’t afford an investment property. But with $320,000 in usable equity, they release a $150,000 split to cover the deposit and costs on a $600,000 investment unit, then take a standalone $480,000 loan against it. They used their home’s growth as the deposit — without touching their savings. Equity made it possible.

Scenario 2: The portfolio builder (equity recycling)

David, 45, owns his home plus one investment property, both having grown in value.

Every few years, as values rise, David releases the new usable equity to fund the next deposit — keeping each loan standalone to avoid cross-collateralisation. He’s built four properties this way over a decade, each purchase funded largely by the growth of the ones before. Disciplined equity recycling at work.

Scenario 3: The over-reacher (a cautionary tale)

Mia releases the maximum equity possible, leaves no buffer, and cross-collateralises everything.

When rates rise and a tenant leaves, she has no cash reserve, can’t cover the shortfall, and — because her loans are tangled — can’t easily sell one property without unwinding the lot. Equity release without buffers and clean structure is dangerous.

Common Mistakes to Avoid

- Releasing every dollar of equity with no cash buffer left over.

- Cross-collateralising properties instead of keeping loans standalone.

- Using redraw / mixed loans without understanding the tax consequences.

- Forgetting serviceability — having the equity but not the borrowing capacity.

- Over-estimating your home’s value before the bank’s valuation confirms it.

- Ignoring cash flow — buying a property you can’t actually afford to hold.

- Not stress-testing for higher rates or vacancies.

- Skipping professional advice on structure and tax.

Strategies for Safely Building a Portfolio with Equity

- Keep loans standalone. Avoid cross-collateralisation so each property can be sold or refinanced independently.

- Use separate loan splits for each equity release, clearly tied to its purpose, for clean tax treatment.

- Always retain a buffer. Never release equity right down to the limit — keep reserves in an offset.

- Pair with offset accounts to stay flexible and reduce interest while keeping cash accessible.

- Buy on fundamentals, not just because you can — the property still has to be a good investment.

- Stay under 80% combined LVR where possible to avoid LMI and keep a safety margin.

- Review annually. As values and rules change, so should your structure.

- Build your team — a portfolio-experienced broker and an investment-focused accountant are essential.

Equity Release Checklist

- ☐ Current home value confirmed (ideally by a lender valuation)

- ☐ Usable equity calculated: (value × 80%) − loan balance

- ☐ Borrowing capacity assessed by a broker (DTI under control)

- ☐ Separate loan split planned for the equity release (clean tax structure)

- ☐ Standalone loan planned against the new property (no cross-collateralisation)

- ☐ Combined LVR kept at/under 80% to avoid LMI (where possible)

- ☐ Cash flow modelled — rent vs all holding costs

- ☐ Buffer retained (several months’ repayments per property)

- ☐ Stress-tested at a higher interest rate

- ☐ Tax structure and 2027 changes reviewed with an accountant

Frequently Asked Questions

How much equity can I use to buy an investment property? Usually up to 80% of your home’s value minus your current loan balance. For a $900,000 home with a $400,000 loan, that’s around $320,000 of usable equity. You can sometimes access more by paying LMI.

Can I use equity instead of a cash deposit? Yes — that’s the core of the strategy. Released equity can fund the deposit and purchasing costs on your next property, so you may not need fresh savings. You still need the borrowing capacity to service the new loan.

What’s the difference between redraw and offset for funding a deposit? Redraw pulls back extra repayments from your loan (and can create tax-deductibility complications). An offset is a separate account holding your own cash that reduces interest. For funding an investment, a clean separate loan split is usually best — confirm with your accountant.

Is releasing equity risky? It increases debt against your home and amplifies both gains and losses. The main risks are over-leverage, falling values, cross-collateralisation and tax mistakes. Buffers, clean loan structure and professional advice manage these.

Will refinancing to release equity affect my tax? The deductibility of the interest depends on what the released funds are used for. Money used to buy an income-producing investment is generally deductible; mixing purposes (e.g. via redraw on your home loan) can complicate this. Always get accounting advice.

Do I need a cash buffer if I’m using equity? Yes — arguably more so. Don’t release equity to the absolute limit. Keep several months’ repayments per property in reserve (ideally in an offset) to handle rate rises and vacancies.

Can I keep using equity to buy multiple properties? Yes — this is “equity recycling.” As each property grows in value, you build new usable equity to fund the next deposit. The constraints are your borrowing capacity, DTI and cash flow, not just available equity.

The Bottom Line: Your Home Is a Launch Pad, Not a Limit

For many Australians, the deposit for their next property isn’t sitting in a savings account — it’s already built into the home they live in. Equity release is how you put that value to work, turning the growth in one property into the deposit for the next, and potentially the foundation of a whole portfolio.

But this is a strategy that rewards structure and discipline. The investors who build wealth with equity keep their loans standalone, retain real buffers, stay within sensible LVR limits, get the tax structure right, and always make sure the cash flow works. The ones who get into trouble release too much, leave no margin, and tangle everything together. The difference between the two is planning — not luck.

Your next step: Do one calculation this week — work out your usable equity ((home value × 80%) − loan balance) and write down the number. Then book a conversation with a portfolio-experienced mortgage broker and an investment-focused accountant to confirm your borrowing capacity and the cleanest structure for your situation — especially with the 2027 tax changes on the horizon. Your home may have already done the hard part of saving your next deposit. The rest is strategy.

Disclaimer: This article is general information only and does not constitute financial, tax, legal or credit advice. It does not take into account your personal circumstances, objectives or needs. Releasing equity increases the debt secured against your home and carries risk, including the risk of loss of property. Interest rates, lending criteria, LVR/LMI thresholds, APRA settings and tax laws change, and figures here (including indicative 2026 rates and the worked examples) are illustrative only. The negative gearing and CGT measures referred to were announced as at the 2026–27 Federal Budget and are not yet law as at the date of writing. Always seek advice from a licensed mortgage broker, financial adviser and/or accountant before releasing equity or making a property investment decision.