Imagine living in the Sydney suburb you actually love — close to the beach, the cafés, your work — while quietly building a property portfolio somewhere more affordable. That’s the promise of rentvesting, and in a city where the median house now pushes toward $1.8 million, it’s why thousands of young Australians are rethinking the old “buy your first home” rulebook.

But does it actually stack up financially? Or is it just a clever way to justify renting forever? The only way to know is with real numbers.

This article puts rentvesting Sydney under the microscope with a full case study — realistic 2026 prices, rents, deposits, stamp duty, mortgage repayments, rental income, tax and cash flow — then compares the 5-year and 10-year wealth outcomes against simply buying a home to live in. We’ll cover what rentvesting is, why it’s booming, the advantages and the very real risks (including one big 2027 tax change), and exactly who it suits. No hype — just the maths. Let’s run the numbers.

What Is Rentvesting?

Rentvesting is a property strategy where you rent the home you live in, while owning an investment property somewhere else.

Instead of buying a place to live (and being limited to what you can afford in the suburbs you want), you:

- Rent in the area you love — often a lifestyle suburb you couldn’t afford to buy in.

- Buy an investment property in a more affordable suburb with strong growth or rental yield, and let tenants help pay it off.

In one sentence: Rentvesting means you rent where you want to live and buy where it makes financial sense — separating your lifestyle decision from your investment decision.

It’s become a popular first home buyer strategy precisely because it breaks the trade-off between “live where I want” and “get onto the property ladder.”

Why Rentvesting Has Become Popular in Sydney

Sydney is the perfect storm for rentvesting, for a few reasons:

- Buying where you want is often impossible. With the house median heading toward ~$1.8 million, buying in inner, eastern or northern Sydney is out of reach for most first-timers.

- But renting there is achievable. A unit in a desirable area might rent for ~$750–$900/week — a fraction of the cost of buying it.

- Affordable growth corridors exist elsewhere. Western and South-Western Sydney (and beyond) offer entry prices around $550,000–$700,000, supercharged by the Western Sydney Airport, new metro lines and major infrastructure.

- The rent-vs-buy gap is huge. In expensive suburbs, it’s often far cheaper to rent than to service a mortgage on the same property — freeing up money to invest.

In short, Sydney property investment maths increasingly favours decoupling where you live from what you own.

Rentvesting vs Buying a Home: The Key Difference

| Buying a home (owner-occupier) | Rentvesting | |

|---|---|---|

| Where you live | A suburb you can afford to buy in | A suburb you want to live in (renting) |

| What you own | The home you live in | An investment property elsewhere |

| Tax | No deductions; no rental income | Rental income + tax-deductible costs |

| First-home concessions | Eligible (stamp duty exemption, grants) | Generally forfeited (you’ve owned property) |

| Flexibility | Tied to one location | Move easily; portfolio not tied to lifestyle |

| Emotional payoff | Security of “your own home” | Lifestyle now + wealth building |

That fourth row is critical and often missed — we’ll see its dollar impact in the case study.

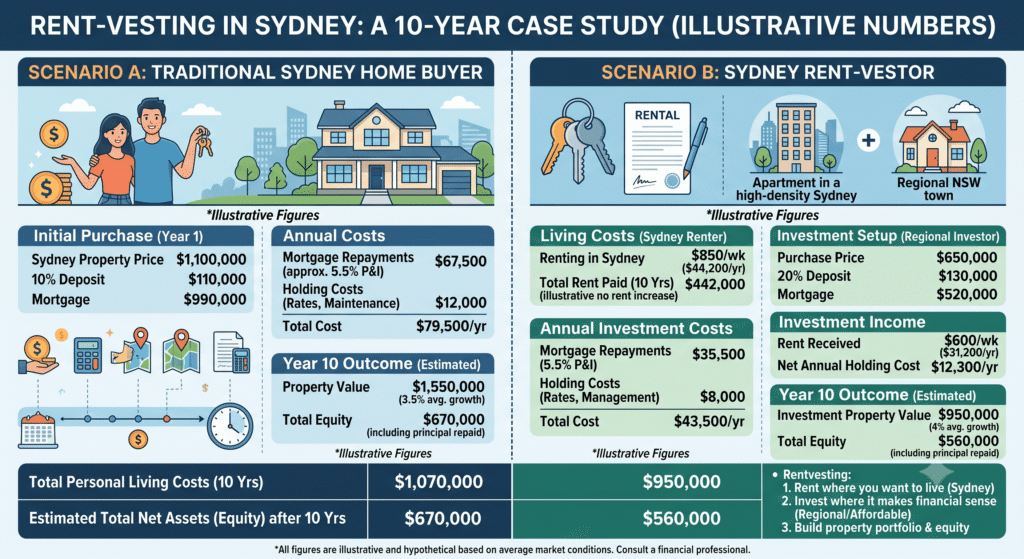

The Case Study: Meet Our Buyers

Let’s follow Jordan and Alex, a couple in their early 30s. (Figures are illustrative, based on indicative 2026 data — always verify your own numbers.)

- Combined income: $140,000

- Savings: $150,000

- First-home buyers (neither has owned property)

- They want to live in a desirable inner-Sydney area, where renting a nice 2-bedroom unit costs about $800/week ($41,600/year), but buying there is unaffordable.

They’re weighing two paths:

- Option A — Buy a home: Purchase a $750,000 home (a unit or outer-suburb house — a compromise on location) to live in.

- Option B — Rentvest: Keep renting their dream-area unit at $800/week, and buy a $650,000 investment property in an affordable Western Sydney growth suburb.

Shared assumptions (illustrative)

- Owner-occupier interest rate: 6.1%; investor rate: 6.6% (2026 indicative)

- Home capital growth: 4%/year (affordable compromise suburb)

- Investment capital growth: 6%/year (genuine growth corridor)

- Investment gross rental yield: 5% (~$625/week, $32,500/year)

Why different growth rates? This is the heart of rentvesting: you buy where the growth is, not where you can afford to live. A growth-corridor investment can reasonably be expected to outpace a compromise owner-occupier suburb. (Growth is never guaranteed — we stress-test this assumption later.)

Upfront Costs Compared

| Cost | Option A: Buy Home ($750k) | Option B: Rentvest ($650k investment) |

|---|---|---|

| Deposit | ~$147,000 (≈20%) | ~$122,000 (≈19%) |

| Stamp duty | $0 (first-home exemption, under $800k) | ~$25,000 (no concession for investors) |

| Other costs (legals, inspection) | ~$3,000 | ~$3,000 |

| Total upfront | ~$150,000 | ~$150,000 |

| Loan amount | ~$603,000 | ~$528,000 |

The stamp duty trap for rentvestors

Notice the difference: Jordan and Alex pay $0 stamp duty if they buy a home (NSW exempts first-home buyers on properties up to $800,000) — but ~$25,000 if they buy an investment instead. As investors, they get no first-home concessions.

Worse, by buying an investment property first, they generally lose their first-home-buyer status for any future home purchase — forfeiting the stamp duty exemption (worth up to ~$31,000), the First Home Guarantee (5% deposit, no LMI), and first-home grants down the track. This is the single most underrated cost of rentvesting, and it must be weighed seriously.

Annual Cash Flow Compared

Now the ongoing money, year one (illustrative):

| Item | Option A: Buy Home | Option B: Rentvest |

|---|---|---|

| Rent paid (where they live) | $0 | $41,600 |

| Loan repayments | $43,600 (P&I) | $34,980 (interest-only) |

| Rates, insurance, maintenance | $6,000 | $7,000 (incl. management) |

| Less: rental income | $0 | −$32,500 |

| Less: tax refund (negative gearing)* | $0 | −$4,600 |

| Net annual cost | ~$49,600 | ~$46,480 |

*Assumes negative gearing applies — see the 2027 warning below.

In this scenario, rentvesting is actually slightly cheaper per year and lets Jordan and Alex live in their dream suburb the whole time. The investment property runs at a modest loss (negatively geared), but rental income and tax benefits cover most of the cost.

How negative gearing helps the rentvestor — and the 2027 warning

Because the investment’s costs (interest + expenses) exceed its rent, it makes a paper loss that — under current rules — is deductible against Jordan and Alex’s salary, generating a tax refund. That’s a core rentvesting advantage homeowners don’t get.

⚠️ Critical 2026 update: In the 2026–27 Federal Budget, the government announced that from 1 July 2027, negative gearing on established residential properties bought after 12 May 2026 will be limited — losses will only offset rental income or capital gains, not salary. New builds are exempt (keeping full negative gearing). These measures are not yet law. The implication for 2026 rentvestors is huge: if Jordan and Alex buy an established investment now, the salary tax refund above largely disappears from July 2027. To preserve it, they’d need to buy a new build — or accept the changed maths. Get current advice from a licensed accountant.

5-Year and 10-Year Wealth Outcomes

Here’s what really matters — how wealth builds over time (illustrative, using the growth assumptions above).

| Outcome | Option A: Buy Home | Option B: Rentvest |

|---|---|---|

| Property value at Year 5 | ~$912,500 | ~$869,800 |

| Loan balance at Year 5 | ~$559,000 (P&I paydown) | ~$528,000 (interest-only) |

| Equity at Year 5 | ~$353,500 | ~$341,800 |

| Property value at Year 10 | ~$1,110,200 | ~$1,164,000 |

| Loan balance at Year 10 | ~$503,000 | ~$528,000 |

| Equity at Year 10 | ~$607,200 | ~$636,000 |

What the numbers show:

- At Year 5, the two paths are remarkably close (~$354k vs ~$342k equity). The homeowner is slightly ahead because they’re paying down principal; the rentvestor (on interest-only) builds equity through growth alone.

- By Year 10, the rentvestor pulls ahead (~$636k vs ~$607k) — because their growth-corridor property (6%) outpaced the compromise home suburb (4%), despite being a cheaper property with no principal paid down.

- And the rentvestor lived in their preferred suburb the entire decade.

The portfolio-scaling advantage

Here’s where rentvesting can really separate from buying a home. By Year 5, Jordan and Alex’s investment is worth ~$870,000 with a $528,000 loan — giving them usable equity of around $168,000 (80% of value minus the loan). They can release that equity to buy a second investment property, accelerating their portfolio.

A homeowner also builds usable equity — but it’s locked in the home they live in, and tapping it adds debt to their own roof. The rentvestor’s equity sits in an investment asset purpose-built for leverage. This is how rentvesting becomes a portfolio-building engine, not just a single-property play.

The honest caveat: These outcomes are highly sensitive to the growth assumptions. If both properties grew at the same rate, the homeowner would likely stay ahead on equity (principal paydown + a bigger property + no rent paid). Rentvesting wins when (a) you’d otherwise be priced out of buying anything you actually want, (b) your investment suburb genuinely outgrows your compromise home suburb, and (c) you use the strategy to scale. Nobody can guarantee growth — model conservatively.

Advantages of Rentvesting

- Live where you want, now — no compromise on lifestyle.

- Buy where it makes sense — chase growth or yield, not just affordability.

- Get onto the ladder sooner — a $650k investment is more attainable than an $1.8M home.

- Tax benefits — deductible costs and (for now / new builds) negative gearing.

- Flexibility — move cities or suburbs easily; your asset isn’t tied to your lifestyle.

- Portfolio potential — release equity to buy again and scale.

Disadvantages and Risks of Rentvesting

- You forfeit first-home concessions — stamp duty exemption, First Home Guarantee, grants (often the biggest hidden cost).

- You’re still renting — subject to rent rises, lease insecurity and landlords’ decisions.

- No emotional security of owning your own home.

- Negative gearing is changing — the 2027 reforms hit established-property tax benefits.

- Capital growth isn’t guaranteed — the whole thesis leans on your investment outperforming.

- Two housing costs to manage — rent plus a mortgage (offset by rental income, but still).

- Discipline required — the cash-flow saving only helps if you invest it, not spend it.

Borrowing Considerations for Rentvestors in 2026

- The 3% serviceability buffer means you’re assessed near ~9.5% — and lenders count both your rent and the investment loan when sizing your capacity.

- The new debt-to-income (DTI) cap (from Feb 2026) limits banks to 20% of loans above 6× income — relevant as you scale.

- Rental income helps — lenders count a portion (often ~80%) of expected rent toward serviceability.

- Your rent counts as an expense in serviceability assessments, which can reduce borrowing capacity compared to an owner-occupier.

- Interest-only is common for rentvestors to maximise cash flow and deductibility — but plan for the reversion to P&I (typically after 5 years).

Who Should Consider Rentvesting? (Checklist)

Rentvesting may suit you if:

- ☐ You want to live somewhere you can’t afford to buy.

- ☐ You’re comfortable renting your home for the foreseeable future.

- ☐ You value lifestyle and flexibility over the security of owning your residence.

- ☐ You’re disciplined enough to invest (not spend) the cash-flow difference.

- ☐ You’re focused on long-term wealth, not the emotional goal of “my own home.”

- ☐ You understand and accept you’ll likely forfeit first-home concessions.

- ☐ You’ve modelled the numbers conservatively and sought professional advice.

If you crave the security of your own home and plan to settle in an affordable area anyway, buying to live in may simply suit you better — and that’s a perfectly valid choice.

Actionable Tips for Rentvestors

- Run your own numbers — use realistic, conservative growth assumptions, not best-case.

- Weigh the first-home concessions you’re giving up — put a dollar figure on it before deciding.

- Target genuine growth or yield suburbs — the strategy lives or dies on your investment outperforming.

- Consider a new build if negative-gearing benefits matter post-2027.

- Keep a cash buffer — several months’ repayments, ideally in an offset.

- Use interest-only wisely — for cash flow, but plan the reversion.

- Reinvest the savings — the rent-vs-buy gap only builds wealth if you actually deploy it.

- Build your team — a portfolio-savvy broker and an investment-focused accountant are essential, especially with the 2027 changes.

Frequently Asked Questions

What is rentvesting in simple terms?

Renting the home you live in while owning an investment property elsewhere — so you live where you want and invest where it makes financial sense.

Is rentvesting a good strategy in Sydney in 2026?

It can be, especially if you’d otherwise be priced out of buying where you want to live, and your investment suburb has strong growth prospects. But you forfeit first-home concessions, you’re still renting, and the 2027 negative-gearing changes affect the tax benefits — so model it carefully.

Do rentvestors pay stamp duty?

Yes — as investors they pay full stamp duty (around $25,000 on a $650,000 NSW property) with no first-home exemption. Confirm current rates with Revenue NSW.

Does rentvesting affect my first-home buyer eligibility?

Generally yes — buying an investment property first means you’ve owned property, so you typically lose first-home buyer status, concessions and the First Home Guarantee for a future home. This is a major consideration.

Is it cheaper to rentvest than to buy a home?

Often the annual cash flow is similar or slightly cheaper when rentvesting (rental income and tax benefits offset costs), as our case study shows — but it depends heavily on prices, rents and rates. The bigger differences are upfront costs, lifestyle and long-term growth.

Will rentvesting build more wealth than buying a home?

Sometimes. In our 10-year case study the rentvestor came out slightly ahead because their growth-corridor property outperformed — but if both grew equally, the homeowner often wins on equity (principal paydown + no rent). Outcomes are very sensitive to growth assumptions.

How do the 2027 tax changes affect rentvesting?

From 1 July 2027 (not yet law), negative gearing on established homes bought after 12 May 2026 will be limited to rental income/capital gains, not salary; new builds are exempt. This reduces a key rentvesting tax benefit for established properties — get current accounting advice.

The Bottom Line: Rentvesting Is a Strategy, Not a Shortcut

So — does rentvesting in Sydney stack up? Our case study shows it genuinely can: comparable (or better) long-term wealth, the freedom to live where you actually want, and a real path to building a portfolio — if the numbers and your discipline line up.

But it’s not a free lunch. You give up first-home concessions worth tens of thousands, you stay a renter, the tax rules are tightening in 2027, and the whole strategy leans on your investment outperforming. Rentvesting rewards the investor who models conservatively, chooses growth suburbs wisely, reinvests the savings, and treats it as a deliberate long-term plan — not a clever excuse to keep renting.

The “right” answer isn’t universal. For some, the security of owning their own home wins. For others, rentvesting Australia-style is the smartest way to have both lifestyle and wealth. The key is running your numbers, honestly.

Your next step: This week, do the one calculation that decides it — work out (1) what you’d pay to rent your dream suburb versus buy there, and (2) the dollar value of the first-home concessions you’d give up by rentvesting. Then sit down with a portfolio-experienced mortgage broker and an investment-focused accountant to model both paths for your real income and goals — especially with the 2027 tax changes looming. The numbers will tell you which path is yours.

Disclaimer: This article is general information only and does not constitute financial, tax, legal or credit advice. It does not take into account your personal circumstances, objectives or needs. All figures — prices, rents, deposits, stamp duty, repayments, tax and projected outcomes — are illustrative and indicative only, based on 2026 data, and are highly sensitive to assumptions (especially capital growth, which is never guaranteed). Stamp duty should be confirmed with Revenue NSW; interest rates, lending criteria and tax laws change. The negative gearing and CGT measures referred to were announced as at the 2026–27 Federal Budget and are not yet law as at the date of writing. Property investment and borrowing carry risk, including the risk of loss. Always seek advice from a licensed mortgage broker, financial adviser and/or accountant before making a property or investment decision.