It’s one of the most important — and most misunderstood — decisions in property investing: whose name does the property actually go in?

Buy in your personal name, a family trust, or a company, and you’re choosing a completely different set of rules for tax, asset protection, borrowing, land tax, and what happens to the property when you die. Get it right and you can save tens of thousands and protect your family’s wealth. Get it wrong and you can trigger unnecessary land tax, kill your borrowing capacity, or pay far more CGT than you needed to.

And in 2026, the stakes just got higher. The May 2026 Federal Budget announced sweeping changes to negative gearing, capital gains tax and — for the first time in decades — a direct tax on family trusts. The old structuring playbook is being rewritten.

This guide explains the three main property ownership structures Australia investors use, in plain English: how each is taxed, who they protect, what they cost, and real examples of when each makes sense for first-home buyers, investors and business owners. We’ll compare them with simple tables and scenarios — no jargon, no assumptions. Let’s work out which one fits you.

Important upfront: Ownership structure is genuinely complex and highly personal. This article gives you the lay of the land so you can have a smart conversation — but the final decision should always be made with a licensed accountant and solicitor who know your full situation.

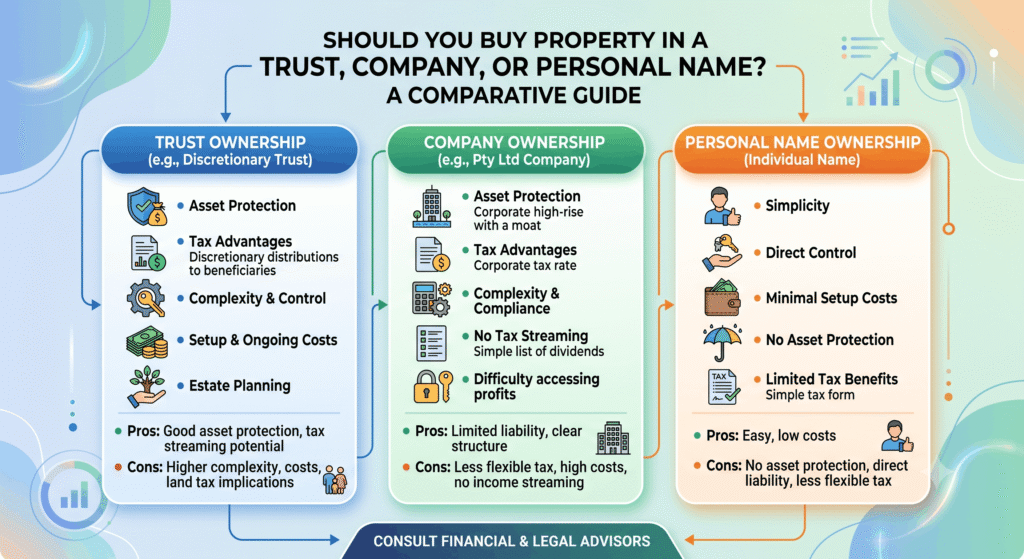

The Three Main Ways to Own Property in Australia

Before we compare, here’s what each structure actually is.

1. Personal name (individual ownership)

You buy the property in your own name (or jointly with a partner). It’s the simplest and most common way — and for most owner-occupiers and many investors, the right one.

2. Family (discretionary) trust

A trust doesn’t “own” anything itself — a trustee holds the property on behalf of beneficiaries (usually family members). A discretionary (family) trust lets the trustee decide each year which beneficiaries receive the income, and how much. This flexibility is why family trust property investment has been popular for decades.

Plain-English definitions:

- Trustee — the person or company that legally controls the trust and its assets.

- Beneficiary — someone who can receive income or capital from the trust.

- Discretionary — the trustee chooses, each year, who gets what.

3. Company

A company is a separate legal entity that buys and owns the property. You own shares in the company. People sometimes buy property in a company name for asset protection or to retain profits at the company tax rate — but, as we’ll see, it has a serious drawback for long-term property investors.

Quick Comparison: The Three Structures

| Feature | Personal Name | Family Trust | Company |

|---|---|---|---|

| Setup cost | Minimal | ~$1,500–$3,000+ | ~$1,000–$2,000+ |

| Ongoing cost | Low | Higher (annual returns, compliance) | Higher (annual returns, ASIC fees) |

| 50% CGT discount | ✅ Yes | ✅ Yes (flows to individuals) | ❌ No |

| Negative gearing vs your salary | ✅ Yes | ❌ No (losses trapped in trust) | ❌ No |

| Income distribution flexibility | ❌ No | ✅ Yes (to beneficiaries) | Limited (dividends) |

| Asset protection | ❌ Weak | ✅ Strong | ✅ Strong |

| Land tax threshold (NSW) | ✅ Yes | ❌ Often none + surcharge | Reduced |

| Borrowing capacity | ✅ Best | ⚠️ Restricted | ⚠️ Restricted |

| Estate planning | Forms part of estate | ✅ Flexible, avoids probate | Via shares |

The pattern: personal name wins on simplicity, tax discounts and borrowing; trusts win on protection and flexibility; companies are a niche tool. Let’s unpack why.

Buying in Your Personal Name

The advantages

- Simplest and cheapest — no setup or extra compliance costs.

- Full 50% CGT discount — hold the property over 12 months and (under current rules) you’re taxed on only half the capital gain.

- Negative gearing against your salary — if the property runs at a loss, you can (currently) deduct it against your other income.

- Best borrowing capacity — lenders treat personal applications most generously, with the widest choice of loans.

- Land tax thresholds — individuals get a tax-free land tax threshold in most states (e.g. NSW), which trusts often don’t.

The disadvantages

- Weak asset protection — if you’re sued or go bankrupt, the property is exposed.

- No income splitting — all the income (and tax) lands on you, at your marginal rate.

- Estate planning limits — the property forms part of your estate, which can mean probate and potential disputes.

Best for: First-home buyers, owner-occupiers, and the majority of everyday investors — especially those who want negative gearing and the CGT discount, and don’t have significant asset-protection risk.

Buying in a Family Trust

The advantages

- Income distribution flexibility — the trustee can stream income to beneficiaries on lower tax rates, potentially reducing the family’s overall tax (this is the classic appeal of property trust Australia strategies).

- Strong asset protection — assets held in trust are generally shielded from personal creditors and bankruptcy.

- Estate planning benefits — trust assets don’t form part of your personal estate, helping avoid probate and pass wealth between generations smoothly.

- Keeps the CGT discount — unlike companies, trusts can pass the 50% CGT discount through to individual beneficiaries (under current rules).

The disadvantages

- Negative gearing is trapped. A loss-making property in a trust can’t be offset against your personal salary. The loss stays inside the trust, carried forward until the trust has income to absorb it. For a negatively geared property, this is a major drawback.

- No land tax threshold (and a surcharge). In NSW, discretionary trusts get no land tax-free threshold and pay an additional 1.6% surcharge. A property with $1,000,000 of land value can cost roughly $16,000+ in annual land tax in a trust, versus potentially zero in personal name if you’re under the threshold. This is the most underestimated cost of trust ownership.

- Harder, costlier borrowing. Fewer lenders offer trust loans, many cap the LVR at 80%, and serviceability is assessed more tightly. At least one major lender paused new trust lending in late 2025, and APRA’s 2026 DTI rules make it harder still.

- Setup and ongoing costs — establishment fees plus annual tax returns and compliance.

Best for: Higher-income earners and families wanting asset protection and income flexibility, holding positively geared or growth properties for the long term — particularly business owners with genuine liability risk.

Buying in a Company

The advantages

- Strong asset protection — like a trust, the company (not you personally) owns the asset.

- Flat company tax rate — profits are taxed at the company rate rather than your (potentially higher) marginal rate, useful for retaining and reinvesting positive cash flow.

- Useful for developers/businesses — where property is part of an active business (e.g. property development), a company can be efficient.

The disadvantages — including the big one

- No 50% CGT discount. This is the dealbreaker for most long-term investors. Companies do not receive the CGT discount that individuals and trusts get — so on a long-held growth property, a company can pay dramatically more tax on the gain.

- Rental income is “passive.” While small businesses can access the 25% base rate company tax rate, that requires no more than 80% of income to be passive. Rental income is passive — so a company holding investment property usually pays the full 30% rate and still gets no CGT discount.

- Double-handling of profits — profits taxed in the company, then again (partly) when paid out as dividends (franking credits offset some of this).

- Restricted, costlier borrowing and ongoing ASIC/compliance costs.

Best for: Property developers, business owners holding premises as part of an active business, or investors focused on positive cash flow they want to retain — rarely the right choice for a passive, long-term capital-growth investor.

⚠️ The 2026 Budget Changes That Reshape This Decision

This is the part that makes 2026 different. The 2026–27 Federal Budget (announced 12 May 2026) introduced reforms that hit all three structures. None of these are law yet — they’re announced measures with future start dates — but they change the calculus.

- Negative gearing limited (from 1 July 2027): For established residential property bought after 7:30pm on 12 May 2026, rental losses will only be deductible against rental income or capital gains — not salary. Properties held before that date are grandfathered; new builds are exempt.

- 50% CGT discount replaced (from 1 July 2027): For individuals, trusts and partnerships, the 50% discount is replaced with cost-base indexation plus a 30% minimum tax on net capital gains (for gains after 1 July 2027). This narrows one of the historic advantages of personal and trust ownership.

- 30% minimum tax on discretionary trusts (from 1 July 2028): This is the headline trust reform. Distributions from discretionary trusts will face a minimum 30% tax — directly targeting the strategy of streaming income to beneficiaries on low marginal rates. It significantly reduces the tax appeal of family trusts.

- Restructure rollover relief (1 July 2027 – 30 June 2030): A three-year window has been flagged to let businesses restructure out of trusts without triggering CGT or stamp duty.

What it means: The traditional reasons to use a family trust for tax minimisation are being curtailed, while its asset protection and estate planning benefits remain. New builds gain a relative tax advantage across structures. Anyone structuring in 2026 must plan with these changes in mind — and this is precisely the moment to get current, qualified advice.

Real Australian Examples

Example 1: The first-home buyer → personal name

Mia, 28, buying her first home to live in.

A trust or company would strip her of the first-home stamp duty exemption, the main residence CGT exemption, the best borrowing rates and the simplest path. There’s no asset-protection need. Personal name, every time.

Example 2: The everyday investor → usually personal name

Tom, 35, buying his first negatively geared investment property on a PAYG salary.

He wants to deduct the loss against his wage and keep the CGT discount — both of which a trust would deny him (the loss would be trapped). With no major liability risk, personal name is almost certainly right, despite what a “set up a trust” sales pitch might suggest.

Example 3: The business owner with risk → family trust

Priya, 48, runs her own business and faces genuine liability exposure, with a high income and adult family members.

For her, asset protection (shielding the property from business creditors) and income flexibility can justify a family trust — particularly for positively geared or growth properties she’ll hold long term. She’ll weigh this against the land tax surcharge, trapped losses, and the 2028 trust tax change with her accountant.

Example 4: The developer → company

David runs a small property development business.

Because development profit is active business income (not passive rent) and he’s reinvesting profits rather than chasing the CGT discount on a long hold, a company structure at the company tax rate can suit his active business. A niche but valid use.

Setup and Ongoing Costs at a Glance

| Personal Name | Family Trust | Company | |

|---|---|---|---|

| Setup | Negligible | ~$1,500–$3,000+ | ~$1,000–$2,000+ |

| Annual compliance | Lowest | Trust tax return + accounting | Company return + ASIC fees |

| Complexity | Simple | Moderate–high | Moderate–high |

Structures aren’t free. The extra cost only makes sense when the protection, flexibility or tax benefit genuinely outweighs it — which, for many everyday investors, it doesn’t.

How to Decide: A Practical Checklist

Work through these with your accountant:

- ☐ Is this your home? → Personal name (keep the main residence exemption and first-home concessions).

- ☐ Is the property negatively geared? → Personal name keeps the loss usable against your salary (trusts trap it).

- ☐ Do you have genuine asset-protection risk (business owner, professional liability)? → A trust or company may be justified.

- ☐ Do you want to split income across family members on lower tax rates? → A trust (but factor the 2028 30% minimum tax).

- ☐ Is it a long-term growth asset? → Avoid a company (no CGT discount).

- ☐ Is it an active business or development? → A company may suit.

- ☐ Have you checked the land tax impact in your state (trust surcharges, no threshold)?

- ☐ Have you priced the borrowing impact (trusts/companies = fewer lenders, tighter terms)?

- ☐ Have you modelled the 2027–2028 tax changes for your situation?

Actionable Tips

- Don’t structure for tax you don’t yet pay. Many investors set up trusts to “save tax” on a property that makes a loss — where a trust actively hurts them by trapping the loss.

- Beware the land tax trap. Run the numbers for your state before choosing a trust — surcharges can quietly cost thousands a year.

- Protect borrowing capacity. If you’re building a portfolio, the lending restrictions on trusts and companies can matter more than the tax angle.

- Match the structure to the property type. New builds, established dwellings, and development sites now have different tax treatment after the 2026 Budget.

- Get advice before you buy. Changing structure later usually triggers stamp duty and CGT — it’s expensive to fix.

- Revisit your strategy as the 2027–2028 reforms become law.

Frequently Asked Questions

Should I buy my first home in a trust or company?

Almost never. Buying your home in your personal name preserves the main residence CGT exemption, first-home concessions and the best borrowing terms. Trusts and companies are for investment/business situations, not your own home.

Is it better to buy an investment property in a trust or personal name?

For most salaried investors with a negatively geared property, personal name is better — you can deduct losses against your salary and keep the CGT discount. Trusts suit those needing asset protection or income flexibility, usually for positively geared or growth properties held long term.

Why don’t companies get the CGT discount?

Under Australian tax law, the 50% CGT discount is available to individuals, trusts and partnerships — but not companies. This makes companies generally unsuitable for long-term capital-growth property, as the eventual tax on the gain can be much higher.

Does a company pay 25% or 30% tax on rental income?

Usually 30%. The 25% base rate applies only if no more than 80% of income is passive — and rental income is passive. A company holding investment property typically fails that test and pays 30%, with no CGT discount.

Do family trusts pay land tax?

Yes, and often more. In NSW, discretionary trusts generally get no land tax-free threshold and pay an extra 1.6% surcharge. Several states apply special trust rates or thresholds. Always check your state before using a trust.

How do the 2026 Budget changes affect trusts?

A 30% minimum tax on discretionary trust distributions is proposed from 1 July 2028, reducing the tax benefit of streaming income to low-rate beneficiaries. The 50% CGT discount is also being replaced from 1 July 2027. Trusts’ asset-protection and estate-planning benefits remain. None of this is law yet — seek current advice.

Can I change my property’s ownership structure later?

You can, but transferring a property between structures generally triggers stamp duty and CGT — making it costly. (A limited restructure rollover relief window for trusts has been flagged for 2027–2030.) This is why getting the structure right before you buy matters so much.

What about an SMSF?

Self-managed super funds can also hold property with potentially lower tax in retirement phase, but come with strict rules, limited access to your money, and high compliance costs. It’s a specialist strategy requiring dedicated advice — beyond the scope of this guide.

The Bottom Line: Structure Around Your Situation, Not a Sales Pitch

There’s no single “best” way to own property in Australia — only the best structure for your circumstances. The honest summary:

- Personal name suits the vast majority — homes, and most everyday investors who want negative gearing, the CGT discount and strong borrowing power.

- Family trusts suit higher-income earners and business owners who genuinely need asset protection or income flexibility, typically for positively geared or long-term growth properties — though the 2028 trust tax change is narrowing the tax case.

- Companies are a niche tool, best for active businesses and developers, and rarely right for passive long-term growth (no CGT discount).

Beware anyone who pushes one structure as a universal “tax hack.” The right choice depends on whether it’s your home, whether the property is positively or negatively geared, your liability risk, your state’s land tax rules, your borrowing plans, and — more than ever in 2026 — the incoming tax reforms.

Your next step: Before you sign anything, write down four things — (1) is this your home or an investment? (2) will it be positively or negatively geared? (3) do you have real asset-protection risk? and (4) what’s your state’s land tax treatment of trusts? Then take those answers to a licensed accountant and solicitor and have them model the structures against the 2027–2028 changes. Getting this right before you buy is one of the highest-value decisions in property investing — and one of the most expensive to fix later.

Disclaimer: This article is general information only and does not constitute financial, tax, legal or accounting advice. It does not take into account your personal circumstances, objectives or needs. Ownership structures have significant legal, tax, land tax, borrowing and estate-planning consequences that vary by state and individual situation. Tax rates, land tax rules and thresholds change, and the figures here are indicative as at 2026. The negative gearing, CGT and trust tax measures referred to were announced as at the 2026–27 Federal Budget and are not yet law as at the date of writing; details and dates may change through legislation. Always seek advice from a licensed accountant, tax agent and/or solicitor before choosing an ownership structure or buying property.