Every Sydney property investor eventually hits the same fork in the road. Do you buy a property that pays you to own it from day one — or one that costs you money each month but could be worth hundreds of thousands more in a decade?

That’s the cash flow versus capital growth question, and in 2026 it matters more than ever. Interest rates rose again early this year, which makes the monthly cost of holding property heavier — and from 1 July 2027, the federal government’s negative gearing and capital gains tax reforms will reshape the maths that drove Sydney investing for decades. Getting this decision right is now central to building a successful Sydney investment property portfolio.

This guide explains the difference between the two strategies in plain English, then identifies and analyses the best Sydney suburbs 2026 for each — with indicative median prices, rental yields, growth drivers, the infrastructure projects reshaping the map, and the risks to watch. Whether you’re chasing income or long-term wealth, by the end you’ll know which path fits you and where to start looking. Let’s dig in.

Cash Flow vs Capital Growth: What’s the Difference?

These are the two engines of property investment Australia-wide. Most properties lean toward one or the other — very few do both brilliantly at once.

What is cash flow investing?

Cash flow investing means buying a property where the rent comfortably covers (or exceeds) the costs of holding it — the loan repayments, rates, insurance, management and maintenance. The property puts money in your pocket, or at least doesn’t drain it.

This is measured by rental yield: the annual rent as a percentage of the property’s price.

Gross rental yield = (annual rent ÷ property price) × 100 Example: a $500,000 unit renting at $550/week earns $28,600 a year — a gross yield of about 5.7%.

Plain-English definition — Positive cash flow: When your rental income is more than all the costs of owning the property, so it pays you to hold it.

What is capital growth investing?

Capital growth investing means buying a property expected to rise significantly in value over time, even if it costs you money to hold along the way. The income matters less; the bet is on the price climbing — building equity you can later use or cash in.

Growth properties typically sit in established or high-demand areas with strong land value, where yields are lower (because prices are high relative to rent) but long-term appreciation has historically been stronger.

Why investors prioritise one over the other

There’s no universally “right” choice — it depends on your income, borrowing capacity, timeline and risk appetite:

- Choose cash flow when your borrowing capacity is tight, you need the property to support itself, or you want income now (common for investors near or in retirement). Positive cash flow also protects your serviceability, helping you keep borrowing as you scale.

- Choose capital growth when you have a strong, stable income that can absorb monthly shortfalls, a long time horizon (10+ years), and the goal of maximising wealth rather than income.

The 2026 twist: With higher interest rates making negatively geared (loss-making) properties more expensive to hold, and the 2027 tax changes narrowing negative gearing on established homes bought after 12 May 2026, cash flow has become more strategically important than during the cheap-money years. Growth still builds the most wealth long term — but the ability to hold through a higher-rate environment is what lets you get there.

The 2026 Sydney Market Backdrop

A quick lay of the land before we get to suburbs.

- Sydney’s median dwelling value sits at roughly $1.24 million, with the house median far higher — Domain has projected it could reach around $1.83 million through 2026.

- 2026 price forecasts from the major banks cluster between +4% and +8% (CBA around +4%, NAB +6%, ANZ +5.8%, Westpac the most bullish near +8%).

- The affordable end is outperforming. Cotality (formerly CoreLogic) data showed Sydney’s lower-priced quartile rising while the top quartile softened in early 2026 — a continuation of a multi-year pattern where affordable corridors beat blue-chip.

- Average yields are tight: roughly 3.1% for houses and 4.4% for units citywide — which is exactly why cash-flow hunters look to specific suburbs and unit markets.

- Population is surging: Greater Sydney added around 75,200 people in 2024–25, much of it landing in the western and south-western corridors.

The infrastructure reshaping the map

No discussion of Sydney’s best suburbs for 2026 is complete without Western Sydney, where a generational infrastructure build is underway:

- Western Sydney International (Nancy-Bird Walton) Airport opens in late October 2026 (with cargo operations from mid-2026) — the centrepiece of a corridor transformation.

- The M12 Motorway opened toll-free on 14 March 2026, slashing drive times from Liverpool, Fairfield and the south-west to the airport.

- Sydney Metro – Western Sydney Airport (23km, six stations from St Marys to Bradfield) is set to open alongside the airport into 2027.

- Bradfield City Centre — NSW’s planned “third CBD” — targets around 200,000 jobs, anchoring the Western Sydney Aerotropolis.

- The South West Growth Area (Austral, Leppington, Oran Park, Catherine Field) is planned for 105,000+ new homes by 2041.

- Further out, Sydney Metro West (Parramatta to the CBD) is due around 2032, supporting the Parramatta–Westmead corridor.

A note on all figures below: Median prices and yields move every quarter and vary by property type and street. Treat the numbers here as indicative, and always verify current data via CoreLogic/Cotality, Domain or PropTrack before buying.

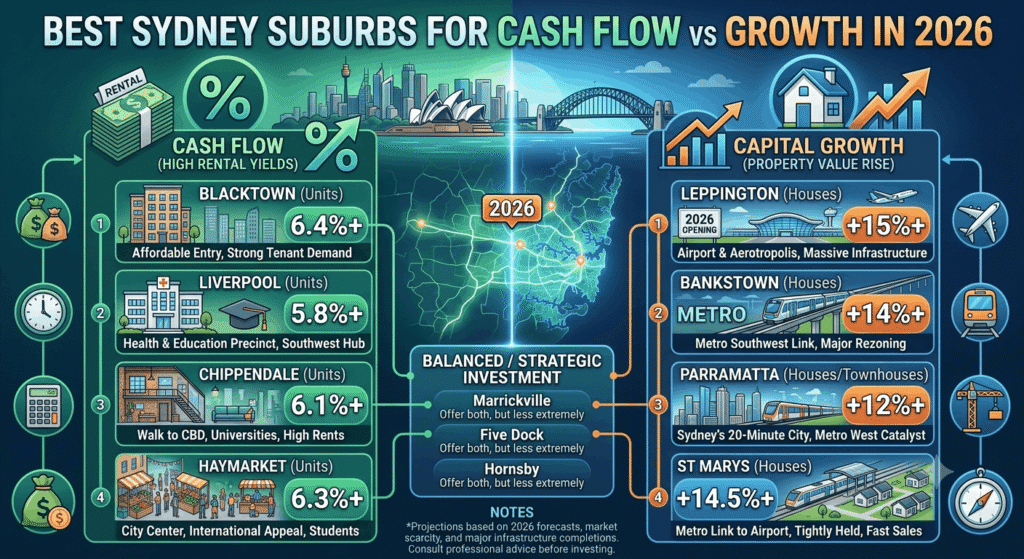

Best Sydney Suburbs for Cash Flow in 2026

For cash flow property Sydney investors, the action is overwhelmingly in Western and South-Western Sydney units — affordable entry prices plus strong, tight rental demand from working families, students and migrant communities. These are areas where the rent works hard relative to the price.

| Suburb | Property type | Indicative price | Indicative gross yield | Why it works |

|---|---|---|---|---|

| Fairfield | Units | ~$356k–$534k | ~6.6% | Affordable, transport links to Parramatta/Liverpool, deep tenant demand |

| Cabramatta | Units | ~$368k–$552k | ~6.3% | Tight rental market, strong family/student demand, near Liverpool jobs |

| Blacktown / Harris Park | Apartments | under ~$500k | ~6.3%+ | Major western hub, low entry price, consistent occupancy |

| Lakemba | Units | Affordable | Strong | Convenience + affordability, reliable rental performance |

| Bankstown / Liverpool | Units | Mid | ~5–6% | Employment hubs, infrastructure, balanced yield + some growth |

What cash-flow suburbs have in common

- Sub-2% vacancy rates — tenants are plentiful, so your income is reliable.

- Affordable entry prices — easier on borrowing capacity, and yields stay high.

- Proximity to jobs and transport — Liverpool, Parramatta and the M12 corridor underpin demand.

- Unit-dominant — units carry higher yields than houses because the rent is high relative to the (lower) price.

The trade-off

Higher-yield units typically deliver slower capital growth than houses, and apartment markets carry oversupply risk in precincts with lots of new high-rise stock. Cash flow keeps you comfortable; it rarely makes you rich on its own.

Best Sydney Suburbs for Capital Growth in 2026

For capital growth suburbs Sydney investors, 2026’s strongest fundamentals line up in three distinct groups.

1. The Western Sydney Airport corridor (the structural growth story)

This is the headline opportunity. The airport, metro, motorways and Bradfield jobs engine are reshaping the south-west, and affordable corridor suburbs have historically outperformed once infrastructure moves from “planned” to “being built.”

Suburbs in and around the South West Growth Area — Leppington, Austral, Oran Park, Catherine Field and the broader Liverpool–Camden–Penrith corridor — sit closest to the action. Bringelly, right next to the airport, has already risen sharply as the build advanced.

- Drivers: ~200,000 future jobs at Bradfield, a new airport, new metro stations, and 105,000+ planned homes drawing population and demand.

- The catch: check the Aircraft Noise Exposure Forecast (ANEF) contours for any property near the airport — noise zones can restrict land use and dent resale value and liveability. Expect years of construction disruption, and don’t overpay for “future” value that’s already priced in.

2. Gentrifying middle-ring suburbs (balance of price and growth)

Established suburbs a little further in offer growth without frontier-style risk. Examples flagged by analysts heading into 2026 include Mount Pritchard (a family-friendly suburb that has seen very strong recent gains), Winston Hills (stability plus infrastructure access), and forecast performers like Mount Annan, Whalan and parts of the Hills district. These reward investors who want appreciation with steadier tenant demand.

3. Blue-chip coastal and North Shore (defensive long-term growth)

At the premium end, Eastern Suburbs (Randwick, Coogee, Bondi) and North Shore suburbs (e.g. Mosman) deliver lower yields but resilient, long-term capital growth, with vacancy rates often below 1% and strong owner-occupier demand. These are defensive holds for high-income investors with the borrowing power to absorb negative cash flow — and they tend to hold value better in downturns.

| Growth segment | Example suburbs | Indicative price point | Yield | Growth driver |

|---|---|---|---|---|

| Airport/SW corridor | Leppington, Austral, Oran Park, Bringelly | Entry–mid (corridor varies) | Moderate | Airport, metro, Bradfield jobs, population |

| Gentrifying middle-ring | Mount Pritchard, Winston Hills, Mount Annan | ~$900k–$1.2M+ | ~3–4% | Gentrification, affordability runway, transport |

| Blue-chip coastal/North Shore | Randwick, Coogee, Bondi, Mosman | $2M–$5M+ (houses) | ~2–3% | Scarcity, prestige, owner-occupier demand |

Cash Flow vs Growth: Side-by-Side

| Factor | Cash Flow Strategy | Capital Growth Strategy |

|---|---|---|

| Goal | Income now | Wealth later |

| Typical yield | 5.5%–6.6%+ | 2%–4% |

| Typical Sydney location | Western/SW units (Fairfield, Cabramatta, Blacktown) | Airport corridor, middle-ring houses, blue-chip coastal |

| Effect on borrowing capacity | Supports it (adds income) | Strains it (monthly shortfall) |

| Best for | Tight budgets, income seekers, scaling portfolios | High earners, long horizons, wealth maximisers |

| Main risk | Slower growth, unit oversupply | Holding costs, affordability ceiling, overpaying for hype |

| 2026/2027 tax angle | More resilient to negative-gearing changes | New builds favoured to retain negative gearing |

Real-World Investor Scenarios

Scenario 1: The first-time investor on a tight budget → cash flow

Sam, 31, has solid savings but limited borrowing capacity at current rates.

A negatively geared house in a blue-chip suburb would stretch Sam thin every month and risk his serviceability. Instead, he buys a ~$480,000 unit in Fairfield yielding around 6.6%. The rent covers most of his costs, the property barely dents his cash flow, and his borrowing capacity stays intact — so he can buy again sooner. Cash flow is the smart entry.

Scenario 2: The high-income professional → capital growth

Priya, 44, earns a strong, stable salary and already owns her home.

Priya can comfortably absorb a monthly shortfall and has a 15-year horizon. She targets a house in a gentrifying middle-ring suburb (or a new build in the airport corridor to retain negative-gearing benefits under the 2027 rules). Lower yield, higher long-term growth — and the tax position works in her favour. Capital growth fits her perfectly.

Scenario 3: The portfolio builder → a balanced blend

Marco, 38, is building a multi-property portfolio over a decade.

Marco mixes both: a couple of high-yield Western Sydney units to keep his portfolio cash-flow positive and his serviceability healthy, paired with one or two growth-focused corridor houses to drive equity. The cash flow keeps the engine running; the growth builds the wealth. A blended strategy is the scalable answer.

Investment Risks to Watch in 2026

Smart investing means managing risk, not ignoring it:

- Higher interest rates. Rates rose in early 2026 — stress-test every purchase above today’s rate and keep a cash buffer.

- Aircraft noise zones. Near the new airport, check ANEF contours before buying; noise can hit liveability and resale.

- Construction disruption. Corridor suburbs are active building sites for years — factor that into liveability and tenant appeal.

- Unit oversupply. High-yield apartment precincts with lots of new stock can see weak growth and softer rents.

- Buying the hype. In corridors where prices have “already tripled,” much of the future may be priced in. Pay for fundamentals, not headlines.

- Affordability ceiling. Sydney is expensive; growth can stall when buyers simply can’t stretch further.

- The 2027 tax reforms. Negative gearing on established homes bought after 12 May 2026 is set to be limited from 1 July 2027 (new builds exempt), and the 50% CGT discount is being replaced — get current advice from a licensed accountant.

- Single-corridor concentration. Don’t put everything in one growth story; diversify property types and locations.

How to Choose the Right Strategy: Actionable Tips

- Start with your borrowing capacity, not the suburb. What you can service decides what’s realistic. A tight budget points to cash flow; strong serviceability opens up growth.

- Match the strategy to your timeline. Need income within a few years? Cash flow. Building wealth over 10+ years? Growth.

- Run the real numbers. Calculate net yield (gross yield minus all costs — and remember net is typically only 60–70% of gross). A “6% yield” can still be cash-flow negative after rates and management.

- Check vacancy rates. Under ~2% signals healthy demand. High vacancy undermines even a great-looking yield.

- Verify data at purchase time. Pull current CoreLogic/Cotality, Domain or PropTrack figures — the numbers in any article (including this one) date quickly.

- Follow the infrastructure, but buy on fundamentals. Jobs, transport and population are the real drivers — not the marketing brochure.

- Consider a blend as you scale. Cash-flow properties keep you serviceable; growth properties build equity. Together they let you keep buying.

- Get professional advice. A portfolio-savvy broker, an investment-focused accountant, and current tax advice (especially given the 2027 changes) are worth far more than they cost.

Frequently Asked Questions

What are the best Sydney suburbs for cash flow in 2026? Western and South-Western Sydney unit markets lead on yield — suburbs like Fairfield, Cabramatta, Blacktown/Harris Park and Lakemba offer indicative gross yields around 6%+, with affordable entry prices and tight rental demand. Always verify current figures before buying.

What are the best Sydney suburbs for capital growth in 2026? The Western Sydney Airport corridor (Leppington, Austral, Oran Park, Bringelly and surrounds), gentrifying middle-ring suburbs (such as Mount Pritchard and Winston Hills), and defensive blue-chip coastal/North Shore areas (Randwick, Coogee, Bondi, Mosman) are the three main growth segments.

Is cash flow or capital growth better in 2026? Neither is universally better. With higher rates and the 2027 tax changes, cash flow has become more strategically important for holding power and serviceability — but capital growth still builds the most long-term wealth. Many investors blend both.

What’s a good rental yield in Sydney? Citywide averages are roughly 3.1% for houses and 4.4% for units. Cash-flow-focused unit suburbs in Western Sydney can reach around 6%+, which is strong for the Sydney market.

Will the Western Sydney Airport boost property prices? It’s a major structural driver — alongside the M12, metro and Bradfield’s ~200,000 future jobs — and corridor suburbs have risen sharply already. But check aircraft noise (ANEF) zones, expect construction disruption, and avoid overpaying for growth that’s already priced in.

How do the 2027 tax changes affect Sydney investors? From 1 July 2027 (not yet law), negative gearing on established homes bought after 12 May 2026 is set to be limited to rental income/capital gains, while new builds keep the benefit; the 50% CGT discount is being replaced. This makes cash flow and new-build strategies more attractive — seek current professional advice.

Should beginners start with cash flow or growth? Beginners with limited borrowing capacity often start with affordable, positive-cash-flow units that support themselves and preserve serviceability for the next purchase — then add growth properties as their position strengthens.

The Bottom Line: Strategy First, Suburb Second

The “cash flow vs growth” debate has no single winner — only the right answer for you. In 2026’s higher-rate, reform-shaped market, the smartest investors are clear-eyed about which engine they’re building:

- Cash flow — Western and South-Western Sydney units (Fairfield, Cabramatta, Blacktown) for income, serviceability and holding power.

- Capital growth — the airport corridor, gentrifying middle-ring houses, and blue-chip coastal for long-term wealth.

- A blend — the scalable path most portfolio builders eventually take.

Sydney’s fundamentals — population growth, supply constraints, and the biggest infrastructure build in the nation’s history out west — remain genuinely compelling. But the suburb is the last decision, not the first. Start with your borrowing capacity, your timeline and your strategy. The right suburb falls out of that.

Your next step: Before you look at a single listing, write down two things — your true borrowing capacity (ask a broker) and whether you need income or growth over the next ten years. Then pick one or two suburbs from this guide that fit, pull their current data, and go inspect. The Sydney market rewards the prepared, not the rushed.

Disclaimer: This article is general information only and does not constitute financial, tax, legal or property advice. It does not take into account your personal circumstances, objectives or needs. Property prices, rental yields, vacancy rates and forecasts are indicative only, drawn from publicly available data as at 2026, and change frequently — verify current figures with CoreLogic/Cotality, Domain or PropTrack before making decisions. Forecasts are projections, not guarantees, and property investment carries risk including the risk of loss. The negative gearing and CGT measures referred to were announced as at the 2026–27 Federal Budget and are not yet law. Always seek advice from a licensed mortgage broker, financial adviser, accountant and/or solicitor before investing.