The Truth About Negative vs Positive Gearing in Australia

For many Australians, property investing feels confusing the moment the term “gearing” enters the conversation.

Should you deliberately lose money to save tax through negative gearing Australia strategies? Or should you aim for strong monthly cash flow with a positively geared property? Why do some high-income earners prefer negatively geared investments while others build portfolios focused entirely on passive income?

In 2026, rising interest rates, tighter lending conditions, increasing rental demand, and changing property prices have made this debate more important than ever.

The reality is this:

Negative gearing and positive gearing are not “good” or “bad.” They are simply different investment strategies with different outcomes around tax, cash flow, borrowing power, and long-term wealth creation.

This guide explains:

- What negative and positive gearing actually mean

- How Australian property tax works in 2026

- Real-world tax calculations and refund examples

- Rental property tax deductions

- Depreciation schedules explained simply

- Cash flow impact of each strategy

- Capital growth vs income investing

- Best strategies for different investor types

- Common mistakes investors make

Whether you are a first-home buyer planning your first investment property or a high-income professional looking to reduce taxable income, this guide will help you understand the full financial picture.

What Is Gearing in Property Investment?

In Australian property investing, “gearing” refers to borrowing money to purchase an investment property.

The property can either:

- Generate a loss each year → Negative gearing

- Generate a profit each year → Positive gearing

- Break even → Neutral gearing

The result depends on:

- Rental income

- Mortgage repayments

- Interest rates

- Maintenance costs

- Depreciation

- Insurance

- Property management fees

- Tax deductions

What Is Negative Gearing?

Negative Gearing Explained

A property is negatively geared when:

The total expenses of owning the property are higher than the rental income earned.

This creates an annual taxable loss.

In Australia, that loss can generally be deducted against your personal income, reducing the amount of tax you pay.

This is why many high-income earners use negative gearing as a 2026 property tax strategy.

Simple Negative Gearing Example

Investment Property

| Item | Annual Amount |

|---|---|

| Rental income | $32,000 |

| Loan interest | $42,000 |

| Property management | $2,500 |

| Council rates | $2,000 |

| Insurance | $1,500 |

| Repairs | $2,500 |

| Depreciation | $6,000 |

Total Expenses

$56,500

Annual Loss

$32,000 – $56,500 = -$24,500

If the investor earns $180,000 salary annually, this loss may reduce taxable income to:

$180,000 – $24,500 = $155,500 taxable income

This reduction can generate a substantial tax refund depending on the investor’s marginal tax rate.

What Is Positive Gearing?

Positive Gearing Explained

A property is positively geared when:

Rental income exceeds all expenses.

This creates positive cash flow and additional taxable income.

Positively geared properties are often popular among investors seeking:

- Monthly passive income

- Better borrowing serviceability

- Faster portfolio scaling

- Reduced financial stress

Simple Positive Gearing Example

| Item | Annual Amount |

|---|---|

| Rental income | $42,000 |

| Loan interest | $22,000 |

| Property management | $2,500 |

| Council rates | $2,000 |

| Insurance | $1,500 |

| Repairs | $2,000 |

| Depreciation | $3,000 |

Total Expenses

$33,000

Annual Profit

$42,000 – $33,000 = $9,000 profit

This $9,000 is added to taxable income and taxed at the investor’s marginal tax rate.

Negative Gearing Australia: Why Investors Use It

Many Australian investors deliberately purchase negatively geared properties because they believe:

- Capital growth will outperform short-term losses

- Tax refunds reduce holding costs

- High-growth suburbs create long-term wealth

- Inflation gradually improves cash flow over time

This strategy is commonly used in:

- Sydney

- Melbourne

- Blue-chip metropolitan suburbs

- High-demand growth corridors

Positive Gearing: Why Cash Flow Matters in 2026

In 2026, many investors are shifting toward positively geared properties due to:

- Higher interest rates

- Cost-of-living pressure

- Lending restrictions

- Rental shortages

- Strong regional rental yields

Positive cash flow improves:

- Borrowing power

- Financial stability

- Portfolio scalability

- Lifestyle flexibility

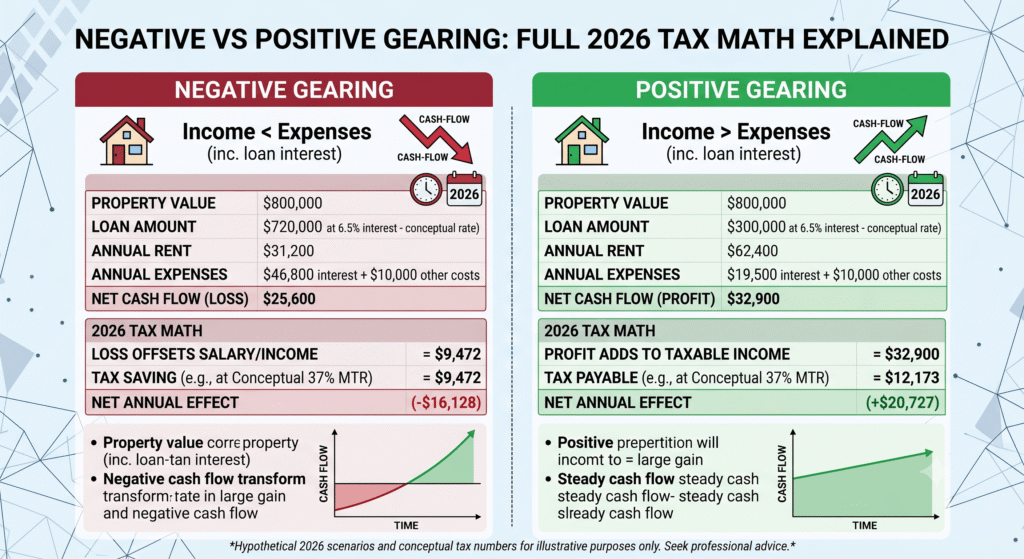

Full 2026 Tax Math: Negative vs Positive Gearing

Scenario 1: High-Income Earner Using Negative Gearing

Investor Profile

| Detail | Value |

|---|---|

| Salary | $220,000 |

| Property Value | $950,000 |

| Loan | $760,000 |

| Interest Rate | 6.2% |

| Rental Income | $39,000 |

Annual Expenses

| Expense | Amount |

|---|---|

| Interest | $47,120 |

| Rates | $2,400 |

| Insurance | $1,800 |

| Property management | $3,200 |

| Repairs | $2,500 |

| Depreciation | $8,000 |

Total Expenses

$65,020

Annual Loss

$39,000 – $65,020 = -$26,020

Tax Savings Calculation

Assuming the investor is in the 45% tax bracket:

$26,020 × 45% = $11,709 tax reduction

Actual Out-of-Pocket Cost

$26,020 loss – $11,709 tax savings = $14,311 real annual cost

This is why many high-income earners tolerate short-term losses for long-term capital growth.

Scenario 2: Positively Geared Regional Investment

Investor Profile

| Detail | Value |

|---|---|

| Salary | $95,000 |

| Property Value | $480,000 |

| Loan | $360,000 |

| Rental Income | $38,000 |

Annual Expenses

| Expense | Amount |

|---|---|

| Interest | $21,600 |

| Rates | $2,000 |

| Insurance | $1,200 |

| Property management | $2,400 |

| Repairs | $1,500 |

| Depreciation | $2,000 |

Total Expenses

$30,700

Annual Profit

$38,000 – $30,700 = $7,300 profit

Tax Payable

Assuming 32.5% marginal tax rate:

$7,300 × 32.5% = $2,372 tax

Net Cash Flow After Tax

$7,300 – $2,372 = $4,928 annual positive cash flow

This investor receives monthly surplus income instead of relying on capital growth.

Negative Gearing vs Positive Gearing Comparison

Quick Comparison Table

| Factor | Negative Gearing | Positive Gearing |

|---|---|---|

| Monthly cash flow | Negative | Positive |

| Tax benefits | High | Lower |

| Risk level | Higher | Lower |

| Capital growth focus | Strong | Moderate |

| Borrowing serviceability | Weaker | Stronger |

| Financial pressure | Higher | Lower |

| Ideal for | High earners | Income-focused investors |

| Portfolio scaling | Slower initially | Faster |

| Lifestyle impact | Requires surplus income | Generates income |

Understanding Rental Property Tax Deductions

Common Investment Property Deductions in Australia

Australian investors can claim many expenses against rental income.

Common deductible expenses include:

- Loan interest

- Property management fees

- Council rates

- Water charges

- Repairs and maintenance

- Insurance

- Land tax

- Depreciation

- Advertising for tenants

- Strata fees

These deductions significantly impact property investment tax Australia calculations.

Depreciation Schedules Explained Simply

What Is Depreciation?

Depreciation allows investors to claim the gradual wear and tear of a property and its fixtures.

This is one of the biggest hidden tax benefits in Australian real estate investing.

Two Main Types of Depreciation

1. Capital Works Depreciation

Applies to:

- Building structure

- Walls

- Roof

- Concrete

- Fixed construction

Usually claimable at 2.5% annually.

2. Plant and Equipment Depreciation

Applies to:

- Air conditioners

- Carpets

- Appliances

- Blinds

- Hot water systems

These often depreciate faster.

Why Depreciation Matters

Depreciation is a “non-cash deduction.”

This means:

You can reduce taxable income without physically spending money each year.

This is why some negatively geared properties still feel manageable financially.

Interest-Only Loans vs Principal-and-Interest Loans

Interest-Only Loans

Many investors use interest-only loans because:

- Repayments are lower

- Tax deductions remain higher

- Cash flow improves short term

However:

- Debt reduces slower

- Long-term interest costs increase

Principal-and-Interest Loans

Benefits include:

- Faster equity growth

- Lower lifetime interest

- Reduced financial risk

But:

- Monthly repayments are higher

- Cash flow may become negative

Offset Accounts and Tax Efficiency

What Is an Offset Account?

An offset account is a bank account linked to a mortgage.

The balance reduces interest charged on the loan.

Example

Loan balance: $700,000

Offset balance: $100,000

Interest is calculated on:

$700,000 – $100,000 = $600,000

This can save thousands annually while preserving tax flexibility.

Capital Growth vs Cash Flow

The Core Investor Debate

Negative gearing investors focus on:

- Long-term capital appreciation

- Wealth creation through equity

- Tax minimisation

Positive gearing investors focus on:

- Immediate income

- Financial independence

- Lower holding risk

Real Wealth Creation Example

Investor A: Negatively Geared Sydney Property

After 10 Years

| Item | Value |

|---|---|

| Purchase Price | $900,000 |

| Value After Growth | $1,550,000 |

| Capital Gain | $650,000 |

Even after years of small annual losses, capital growth creates substantial wealth.

Investor B: Positively Geared Regional Portfolio

After 10 Years

| Item | Value |

|---|---|

| Annual Net Cash Flow | $18,000 |

| Total Cash Flow Over 10 Years | $180,000 |

| Moderate Capital Growth | $250,000 |

This strategy generates lifestyle income earlier.

Capital Gains Tax (CGT) Explained

When an investment property is sold for profit, investors may pay Capital Gains Tax.

50% CGT Discount

If held longer than 12 months:

- Individuals generally receive a 50% discount on taxable capital gains.

Example

Capital gain: $300,000

Taxable gain after discount:

$300,000 × 50% = $150,000 taxable

This amount is added to annual income and taxed accordingly.

Best Strategy for Different Investor Types

Best Strategy for High-Income Earners

Usually Better:

- Negative gearing

- High-growth suburbs

- Tax minimisation strategies

Ideal for:

- Doctors

- Executives

- IT professionals

- Business owners

Best Strategy for First-Home Buyers

Usually Better:

- Neutral or slightly positive cash flow

- Lower risk investing

- Strong affordability focus

This reduces financial stress while learning property investing basics.

Best Strategy for Retirees

Usually Better:

- Positive gearing

- Passive income generation

- Lower debt

Focus shifts from growth to cash flow stability.

Best Strategy for Portfolio Builders

Hybrid Strategy Often Works Best

Many experienced investors combine:

- High-growth negatively geared assets

- Positively geared cash-flow properties

This balances:

- Equity growth

- Borrowing capacity

- Lifestyle flexibility

Pros and Cons of Negative Gearing

Advantages

- Reduces taxable income

- Supports long-term capital growth

- May accelerate wealth creation

- Useful for high-income earners

- Strong tax deductions

Disadvantages

- Ongoing cash losses

- Higher financial stress

- Interest rate risk

- Reduced borrowing capacity

- Reliance on capital growth

Pros and Cons of Positive Gearing

Advantages

- Positive monthly cash flow

- Lower financial risk

- Better loan serviceability

- Easier portfolio scalability

- Improved lifestyle flexibility

Disadvantages

- Higher taxable income

- Potentially slower capital growth

- Fewer tax benefits

- Some high-yield areas have weaker long-term appreciation

Common Property Investment Mistakes

1. Buying Solely for Tax Refunds

A tax refund does not magically make a bad investment profitable.

2. Ignoring Cash Flow

Many investors underestimate:

- Interest rate rises

- Vacancy periods

- Maintenance costs

3. Overestimating Capital Growth

Past performance does not guarantee future growth.

4. Not Using Depreciation Reports

Many investors miss thousands in legal deductions annually.

5. Poor Loan Structuring

Incorrect loan setups can reduce future tax efficiency.

Frequently Asked Questions

Is negative gearing still worth it in 2026?

It depends on:

- Your income level

- Risk tolerance

- Investment timeline

- Cash flow position

- Growth expectations

For high-income earners targeting long-term capital growth, it can still be highly effective.

Is positive gearing safer?

Generally yes.

Positive cash flow reduces financial pressure and helps investors survive market fluctuations more comfortably.

Can a property become positively geared later?

Yes.

Many negatively geared properties gradually become positively geared as:

- Rent increases

- Loan balances decrease

- Inflation improves income

- Interest rates fall

Do tax deductions mean the property is profitable?

No.

Tax deductions reduce losses but do not eliminate them entirely.

What is better: capital growth or cash flow?

Neither is universally better.

The best strategy depends on:

- Income

- Age

- Risk profile

- Financial goals

- Borrowing power

Final Thoughts: Choosing the Right Property Investment Strategy

The debate around negative vs positive gearing is ultimately about balancing:

- Cash flow

- Tax efficiency

- Risk

- Wealth creation

- Lifestyle goals

Negative gearing can create enormous long-term wealth when paired with strong capital growth and disciplined financial management.

Positive gearing can create financial freedom, lower stress, and scalable passive income.

The smartest investors usually avoid extremes.

Instead, they build portfolios strategically using a mix of:

- Growth assets

- Cash-flow properties

- Tax planning

- Smart loan structures

- Long-term wealth principles

Before buying any investment property, carefully assess:

- Your cash flow

- Tax bracket

- Borrowing capacity

- Risk tolerance

- Investment horizon

And most importantly:

Never buy a property purely for tax savings. Buy assets that align with your long-term financial goals.

Ready to Build a Smarter 2026 Property Investment Strategy?

Speak with a qualified mortgage broker, accountant, and property investment advisor before making major investment decisions. The right structure today can save hundreds of thousands in tax, interest, and missed opportunities over the next decade.